Conceptual massing study — Ambassador Commons, 1472 Princess Street, Kingston, Ontario

Development Case Study

1472 Princess Street, Kingston, Ontario — 78 Units, 3 Storeys

The housing market in Kingston is failing working families. In the following case study I will argue how this does not need to continue.

Ambassador Commons is a real site, modelled with real numbers. It demonstrates that a municipally-owned housing corporation can develop, finance, and operate a residential building at below-market rents and still generate a growing annual surplus that flows back to the city permanently.

This is not a subsidy. This is an investment. One that pays the city back in perpetuity.

The model has a 5% vacancy allowance. This is a conservative assumption given Kingston's historically tight rental market and the below-market rent structure, which tends to minimize turnover and maintain waitlists. In practice, vacancy may be lower, but the model does not assume it.

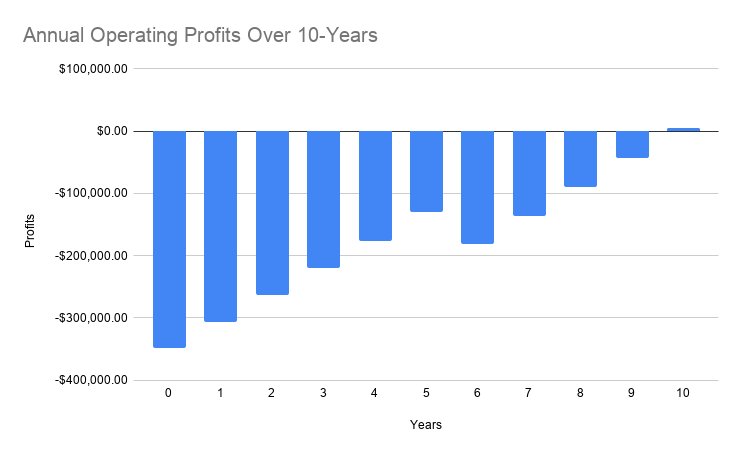

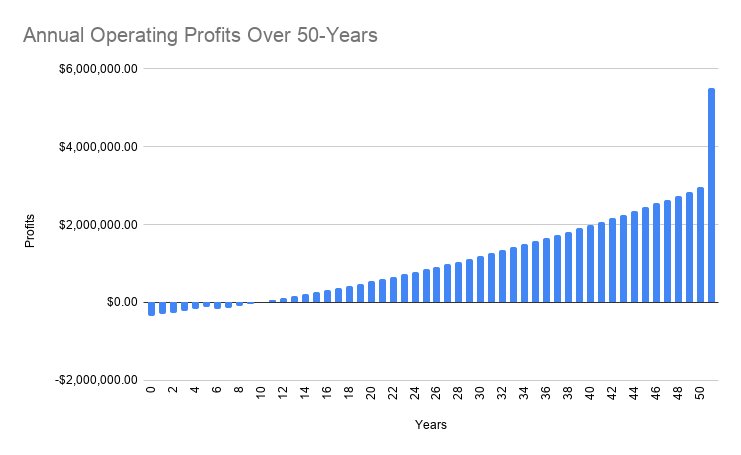

Two construction cost scenarios are presented: $300 per square foot of structure, which is profitable from year one, and $350 per square foot, which runs a modest deficit in early years before turning positive as rent inflation outpaces fixed debt service. Both scenarios converge near $6,000,000 in annual operating profit by year 50 at which point the mortgage is retired and the building is essentially a pure revenue asset for Kingston. This means that even in a worst-case development scenario with overruns and inefficiencies, in the long run the city will still end up with a positive revenue generator.

Development Assumptions

A Note on Operating Costs

Common Area Maintenance (CAM) is modelled in two phases. For the first five years, CAM is set at $3.75 per square foot annually, reflecting the low maintenance demands of a new building under manufacturer and contractor warranty. At year five, CAM steps up to $4.50 per square foot annually, accounting for the transition to self-funded maintenance as major product warranties expire on HVAC systems, building envelope components, and appliances.

Both rates escalate at 2% per year in line with general inflation. The reserve fund contribution is included within these figures. The step-up at year five creates a visible dip in operating surplus on the charts; this is intentional and accurate, not an error.

Rental Rate Comparison

Rates are set below current Kingston market averages while still generating a positive operating surplus. Market rates sourced from active Kingston listings.

| Unit Type | Market Rate ($/sqft) | Ambassador Commons ($/sqft) | Discount |

|---|---|---|---|

| 1-Bedroom | $29.03 | $28.00 | −3.5% |

| 2-Bedroom | $25.52 | $24.00 | −6.0% |

| 3-Bedroom | $24.54 | $23.00 | −6.3% |

| 4-Bedroom | $23.50 | $22.00 | −6.4% |

Monthly income at base rates: $209,786 (after 5% vacancy allowance). All rents grow at 2% annually in the model.

Scenario Comparison

Operating Profit Projections

Annual operating profit shown across 10, 20, and 50-year horizons for both scenarios. The 50-year view reflects the true value of a generational public asset as inflation slowly drives down the impact of debt servicing with a spike in revenues when principal is repaid.

10-Year View

20-Year View

50-Year View

10-Year View

20-Year View

50-Year View

What This Means for Kingston

Ambassador Commons is one building on one site. But it demonstrates something important: the math works. A municipally-owned housing corporation can borrow at rates private developers cannot access, eliminate the profit margin that drives up private rents, and still operate in surplus. All this while offering tenants rents meaningfully below what the market demands.

Now imagine ten buildings. Twenty. The Cataraqui Bay master planned community. Each iteration more efficient and cost-effective than the last as the construction model is standardized, and these savings can get passed down to the tenants with even lower rental rates. Each iteration is a permanent asset on the city's balance sheet, generating revenue that reduces pressure on property taxes for every Kingston resident, homeowner or renter.